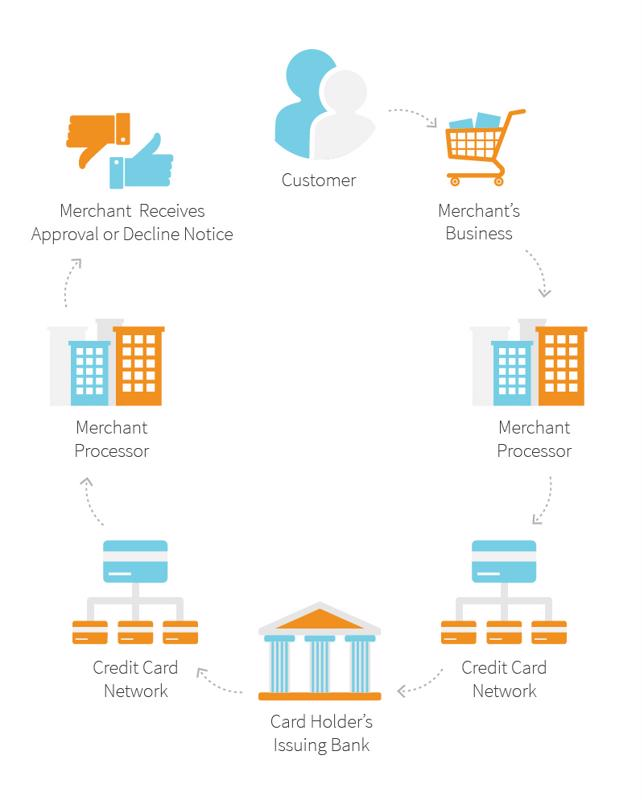

Apple Card payment processing is evolving as Visa has made an aggressive move by offering $100 million to take over the credit card transactions, which would replace Mastercard as the processing network. This transition comes at a pivotal time for Apple, as it seeks to distance itself from Goldman Sachs, which has decided to exit the consumer lending market. The competition among major financial institutions is heating up, with American Express also seeking a piece of the action in this lucrative credit card deal. As payment processing networks undergo these transformations, Apple aims to boost its profitability through enhanced customer loyalty and innovation in payment solutions. The shift in Apple Card payment processing not only highlights the strategic maneuvers of major players but also poses questions about the future of consumer finance in a rapidly changing digital landscape.

The recent developments surrounding Apple’s credit card payment arrangements signify a crucial shift in the financial ecosystem. By inviting Visa into the fold, Apple is reshaping how its users will interact with digital payment solutions and retail transactions. The transition from Goldman Sachs as the primary issuer suggests that Apple is keen on refining its approach to consumer credit and payment management. As we delve deeper into Apple’s financial endeavors, it becomes evident that the integration of advanced payment systems and partnerships with established credit networks can significantly alter the digital finance landscape. Moreover, by understanding these shifts, consumers can better navigate their options within a saturation of available credit card deals.

Understanding the Visa Apple Card Deal

Visa’s recent offer to pay $100 million to Apple for the Apple Card’s payment processing rights has significant implications in the credit card sector. This strategic move aims to position Visa ahead of its rival, Mastercard, as Apple transitions away from its partnership with Goldman Sachs. Such a deal would not only enhance Visa’s portfolio but also potentially boost competition in the payment processing market. With an increasing number of consumers leaning towards digital payments, the collaboration with a tech giant like Apple could further solidify Visa’s dominance in credit card transactions.

This deal highlights a key trend within the financial industry, where major players like Visa and Mastercard are keen to secure partnerships with innovative companies. The entry of technology firms into finance is reshaping traditional banking and payment models. The existing competition among these payment processing networks is fierce; however, a partnership with Apple could provide Visa with invaluable insights into consumer behavior and spending patterns, which could be leveraged for future advancements in payment technology.

The Impact of Mastercard’s Efforts

Mastercard’s attempt to retain the payment processing rights for the Apple Card emphasizes the competitive landscape of credit card deals. As big banks and financial networks vie for lucrative partnerships, Mastercard is not only defending its current position but also strategizing on how to counter Visa’s aggressive bid. Their focus on customer loyalty programs and enhanced benefits could be tactics aimed at sealing their relationship with Apple.

The rivalry between the two networks could lead to improved offers for consumers, as both Visa and Mastercard scramble to enhance their services. With consumers increasingly demanding better rewards and lower fees, the competition spurred by this potential Visa-Apple collaboration could prompt Mastercard to innovate, driving advancements not just within the Apple Card framework but across the entire industry.

Goldman Sachs Exiting Consumer Lending

Goldman Sachs’ decision to exit the consumer lending business signifies a strategic pivot for the financial institution. This move comes in light of the challenges faced while issuing the Apple Card, particularly with customers who have lower credit scores. Such a retreat raises questions about the viability of risk-heavy lending practices and highlights the necessity for financial institutions to reassess their consumer finance strategies, especially in the face of increasing competition from FinTech companies.

In addition, Goldman’s departure could potentially clear the way for more effective management of the Apple Card. New partnerships might lead to enhanced consumer experiences and increased profits from credit card transactions. For any new issuer, the focus will be on harnessing the substantial balances held by Apple Card users—an estimated $20 billion—which could offer significant revenue potential with the right strategies.

Navigating Financial Relationships in Consumer Financing

As Apple positions itself as a formidable player in consumer finance, its relationships with major banks and payment processors have become increasingly complex. Financial institutions have historically been cautious about Apple’s ambitions, given its desire to control every aspect of its ecosystem. This dynamic creates a duality where banks are challenged by competition yet find value in collaboration with one of the world’s leading technology companies.

Maintaining this balance is crucial for banks that want to capitalize on Apple’s vast consumer base. Developing symbiotic relationships with Apple can allow traditional banks to innovate and keep pace with technology while providing superior customer offerings. As Apple expands its grasp in financial services, how banks adapt will determine the landscape of consumer finance in the years to come.

Challenges Faced by Apple Card Users

Apple Card users have faced numerous challenges, leading to regulatory scrutiny and fines for Apple and Goldman Sachs. The zero-interest financing scheme, initially presented as a significant benefit, proved confusing for many cardholders. Inadequate customer support and unclear terms have resulted in consumers feeling misled, reflecting the complexities involved in launching new financial products. This situation illustrates the importance of transparent communication in the financial sector and how fintech companies must address consumer concerns effectively.

Furthermore, the complexities faced by Apple Card users underscore the necessity for rigorous compliance frameworks in consumer finance. As financial products evolve, ensuring that users fully understand their rights and responsibilities remains paramount. The lessons learned from the Apple Card’s launch might serve as valuable insights for other fintech startups looking to penetrate the competitive credit card market.

Comparing the Apple Card to Other Credit Cards

Though the Apple Card has garnered attention for its sleek design and integration with Apple Pay, it is essential to compare its offerings against other available credit cards. Many other cards provide more substantial benefits, including purchase protection, concierge services, and travel rewards without the need for an iPhone. Consumers frequently seek the best value for their spending, and the complexities tied to Apple’s ecosystem might deter potential cardholders from choosing the Apple Card.

Moreover, while the cashback offerings of the Apple Card appear attractive, they fall short compared to other cards that deliver similar or superior rewards without limitations. As digital banking evolves, consumers are likely to prioritize flexibility and broader benefits, challenging Apple to enhance its credit card offerings to remain competitive in a market filled with lucrative alternatives.

The Future of Apple’s Payment Processing Infrastructure

Apple’s move towards managing its payment processing infrastructure reflects a broader trend where tech companies aspire to integrate more deeply into financial services. Should Apple take control of its payment processing, this shift could disrupt the traditional roles of payment processors, leading to innovation and possibly lower transaction fees for consumers. With the increasing reliance on digital payment methods, Apple’s initiative may reshape how payment systems function globally.

However, this shift raises questions about competition and collaboration within the financial industry. As Apple consolidates its grips on payment systems, challenges will arise for existing networks that must adapt to this new landscape. The outcome could redefine power dynamics in finance, compelling banks and payment processors to innovate continuously or risk obsolescence.

The Implications of the Consumer Financial Protection Bureau’s Fine

The $89 million penalty imposed on Apple and Goldman Sachs by the Consumer Financial Protection Bureau (CFPB) sheds light on the challenges that come with regulatory compliance in the financial sector. As fintech companies strive to innovate, they must also adhere to stringent regulations that protect consumers. This incident emphasizes the importance of both transparency and accountability in consumer finance, particularly for companies like Apple that venture into new financial territories.

Furthermore, the penalty reflects broader issues surrounding consumer understanding of financial products, particularly those with complexities such as the Apple Card’s zero-interest financing. Financial institutions must prioritize consumer education and clear communication to avoid potential misinterpretations that can lead to regulatory scrutiny and damage to their reputation.

User Sentiments and Market Trends in the Credit Card Sector

User sentiments regarding the Apple Card and the booming credit card market indicate a desire for improved benefits and customer service. Many consumers expect credit cards to provide not just payment solutions, but also rewards and added-value services. As the market evolves, understanding these sentiments will be crucial for both fintech companies and traditional banks, as they design their products to meet consumer needs.

Analysts note that as users become more educated about available credit card options, their expectations increase. This growing awareness may push financial institutions to adopt more consumer-friendly policies, promoting transparent communication, better rewards, and innovative features that resonate with tech-savvy customers. The competitive landscape, driven by user feedback, will likely encourage both established players and emerging fintechs to prioritize customer satisfaction.

Frequently Asked Questions

How does Apple Card payment processing work with Visa and Mastercard?

Apple Card payment processing utilizes Visa and Mastercard networks to facilitate transactions. Currently, there are discussions of Visa offering $100 million to Apple to take over Mastercard’s role in processing for the Apple Card as it transitions away from Goldman Sachs.

What recent developments are affecting Apple Card payment processing?

Recent news indicates that Apple is moving to replace Goldman Sachs in its credit card venture, spurred by Goldman’s exit from consumer lending due to financial losses. This shift is prompting major players like Visa and American Express to compete for the Apple Card payment processing deal.

Will the transition away from Goldman Sachs impact Apple Card users?

Yes, the transition from Goldman Sachs to a new payment processor could significantly impact Apple Card users, particularly regarding transaction processing efficiency and potential financial offers once a new processor like Visa or American Express assumes control.

What problems led to the Goldman Sachs exit from Apple Card payment processing?

Goldman Sachs faced challenges such as issuing Apple Cards to customers with low credit scores and the inability to charge annual fees. These factors contributed to financial losses and ultimately led to their decision to exit the consumer lending business, impacting Apple Card payment processing.

What are the cashback rewards for Apple Card transactions compared to other credit card deals?

Apple Card offers 2% cashback on transactions made through Apple Pay, with some merchants providing 3% back. However, for physical card transactions, users only receive 1% cashback, which may not compare favorably to other credit card deals that offer better rewards without restrictions.

How can Apple Card users ensure they maximize their payment processing benefits?

To maximize benefits, Apple Card users should primarily use Apple Pay for transactions to earn the highest cashback percentage. Additionally, staying informed about changes in the payment processing landscape, such as shifts from Goldman Sachs to companies like Visa, can help users strategically manage their credit card usage.

What consequences did Apple and Goldman Sachs face related to Apple Card payment processing?

Apple and Goldman Sachs faced an $89 million fine from the Consumer Financial Protection Bureau due to inadequate customer support and unclear terms regarding zero-interest financing with the Apple Card. These issues may have influenced Apple’s decisions around future payment processing partnerships.

Is the Apple Card a competitive option among credit cards when considering payment processing?

While the Apple Card provides decent cashback benefits, it may not be the best option compared to other credit cards that offer similar or better rewards without being tied to the Apple ecosystem. Users seeking comprehensive perks and protections should consider their options in the broader credit card market.

| Key Point | Details |

|---|---|

| Visa’s Offer | Visa proposed to pay Apple $100 million to handle payment processing for the Apple Card, replacing Mastercard. |

| Goldman Sachs Exit | Goldman Sachs is exiting consumer lending, prompting Apple to seek a new banking partner. |

| American Express Competition | American Express is also interested in taking over the payment processing role. |

| Apple Card’s Value | Apple Card users hold $20 billion in balances, indicating potential profitability for the new payment processor. |

| Customer Concerns | Previous issues with cardholder support and confusion over zero-interest financing have led to fines for Apple and Goldman. |

| Market Competition | The relationship between Apple and financial institutions is complex, involving both competition and collaboration. |

| Cashback Benefits | The Apple Card offers 2% cashback with Apple Pay; however, other cards provide better benefits. |

Summary

Apple Card payment processing is set to undergo significant changes, as Visa’s offer to take over from Mastercard signals a pivot in Apple’s financial services strategy. This move comes amid Goldman Sachs’ decision to exit consumer lending, raising important questions about the future of Apple’s credit offerings. The competition among major financial institutions, coupled with the need for improved customer support and benefits, illustrates the evolving landscape of credit card offerings and the necessity for Apple to optimize its position in consumer finance.